Things about Chapter 7 Vs Chapter 13 Bankruptcy

Things about Chapter 7 Vs Chapter 13 Bankruptcy

Blog Article

Top Guidelines Of Bankruptcy Lawyer Tulsa

Table of ContentsThe Ultimate Guide To Experienced Bankruptcy Lawyer TulsaThe smart Trick of Chapter 7 Bankruptcy Attorney Tulsa That Nobody is DiscussingNot known Details About Experienced Bankruptcy Lawyer Tulsa 10 Easy Facts About Which Type Of Bankruptcy Should You File ExplainedThe Best Strategy To Use For Bankruptcy Law Firm Tulsa Ok

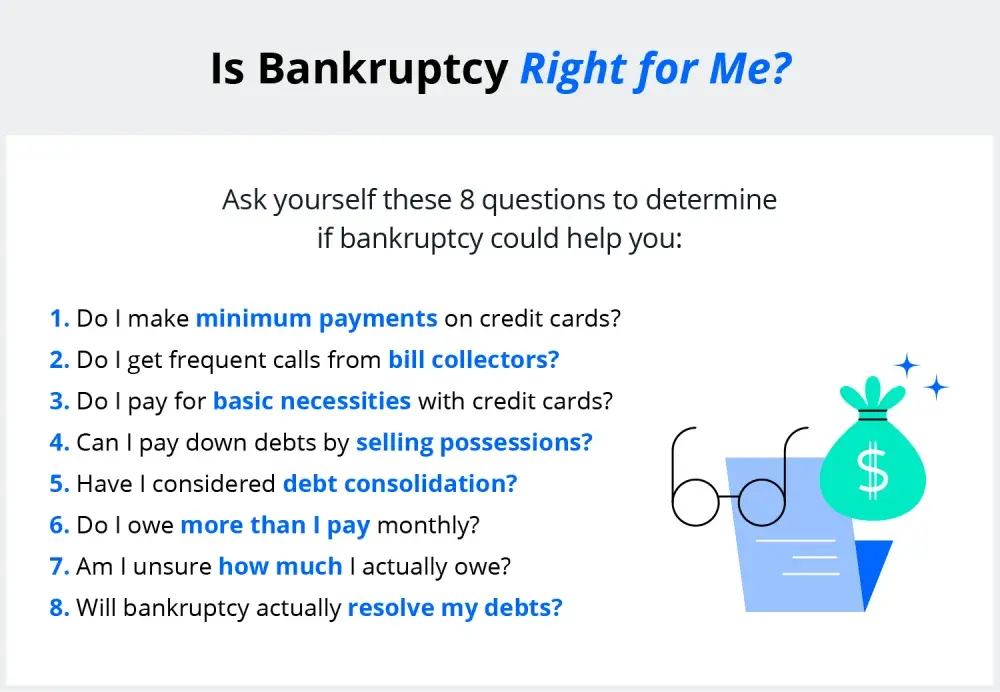

The stats for the other main type, Chapter 13, are even worse for pro se filers. (We break down the distinctions between the two key ins deepness listed below.) Suffice it to claim, speak to a lawyer or 2 near you who's experienced with personal bankruptcy law. Here are a few sources to discover them: It's reasonable that you may be reluctant to pay for an attorney when you're currently under significant financial pressure.Numerous lawyers likewise provide complimentary assessments or email Q&A s. Take benefit of that. (The charitable app Upsolve can assist you discover free appointments, resources and legal assistance cost free.) Ask if insolvency is indeed the right selection for your scenario and whether they think you'll qualify. Before you pay to submit bankruptcy forms and blemish your credit score report for approximately one decade, inspect to see if you have any viable alternatives like financial obligation negotiation or charitable credit scores therapy.

Advertisements by Cash. We might be made up if you click this ad. Ad Now that you have actually decided insolvency is certainly the right strategy and you with any luck removed it with a lawyer you'll need to start on the documents. Prior to you dive into all the main bankruptcy forms, you should get your very own files in order.

The 7-Minute Rule for Chapter 7 Vs Chapter 13 Bankruptcy

Later on down the line, you'll in fact need to verify that by revealing all kind of info concerning your monetary affairs. Below's a standard checklist of what you'll require when traveling in advance: Identifying papers like your vehicle driver's certificate and Social Safety card Tax obligation returns (approximately the past 4 years) Proof of income (pay stubs, W-2s, freelance revenues, income from possessions in addition to any kind of earnings from federal government benefits) Financial institution statements and/or retired life account statements Evidence of worth of your possessions, such as car and genuine estate valuation.

You'll intend to understand what sort of financial obligation you're trying to deal with. Debts like youngster support, spousal support and particular tax debts can't be discharged (and personal bankruptcy can not halt wage garnishment associated to those financial obligations). Trainee lending financial obligation, on the other hand, is not difficult to release, yet note that it is tough to do so (Tulsa OK bankruptcy attorney).

You'll intend to understand what sort of financial obligation you're trying to deal with. Debts like youngster support, spousal support and particular tax debts can't be discharged (and personal bankruptcy can not halt wage garnishment associated to those financial obligations). Trainee lending financial obligation, on the other hand, is not difficult to release, yet note that it is tough to do so (Tulsa OK bankruptcy attorney).If your revenue is too expensive, you have one more alternative: Chapter 13. This option takes longer to solve your financial debts since it calls for a long-term payment strategy generally three to five years prior to several of your remaining financial obligations are cleaned away. The declaring procedure is also a lot much more complicated than Phase 7.

The Tulsa Bankruptcy Consultation Ideas

A Phase 7 personal bankruptcy stays on your credit report for 10 years, whereas a Phase 13 personal bankruptcy drops off after 7. Prior to you submit your bankruptcy types, you have to initially finish an obligatory training course from a credit therapy agency that navigate to this web-site has been approved by the Division of Justice (with the notable exemption of filers in Alabama or North Carolina).

The course can be completed online, in individual or over the phone. You have to complete the training course within 180 days of filing for bankruptcy.

The Ultimate Guide To Best Bankruptcy Attorney Tulsa

Examine that you're submitting with the correct one based on where you live. If your irreversible important source house has actually moved within 180 days of filling, you should submit in the area where you lived the greater portion of that 180-day duration.

Typically, your insolvency lawyer will function with the trustee, but you may need to send the person files such as pay stubs, tax obligation returns, and financial institution account and credit history card declarations straight. A common false impression with personal bankruptcy is that once you submit, you can quit paying your financial obligations. While bankruptcy can help you wipe out many of your unprotected debts, such as overdue clinical costs or individual fundings, you'll want to maintain paying your monthly settlements for guaranteed debts if you want to keep the property.

The Main Principles Of Tulsa Debt Relief Attorney

If you go to risk of repossession and have worn down all various other financial-relief alternatives, then filing for Chapter 13 might postpone the repossession and conserve your home. Inevitably, you will certainly still require the earnings to continue making future home mortgage settlements, along with settling any type of late payments throughout your payment strategy.

If so, you may be required to provide additional details. The audit could postpone any kind of financial obligation relief by numerous weeks. Obviously, if the audit shows up wrong information, your instance might be dismissed. All that said, these are fairly uncommon instances. That you made it this far in the process is a suitable indicator at least a few of your financial obligations are eligible for discharge.

Report this page